The rules that govern how life insurers handle claims in Australia are being rewritten. An independent review of the Life Insurance Code of Practice — the industry's promise on how quickly claims are decided and how claimants are kept informed — is due to report to the Council of Australian Life Insurers (CALI) on 30 June 2026. The incorporation of these recommendations will form what people in the industry are referring to as "LICOP 3.0."

The review matters because it lands at a moment when the data on claims handling is under strain: claims delays are the single most-complained-about issue in financial services, the Code's own compliance committee is recording rising breaches, and the corporate regulator has just secured its largest claims-handling penalty to date. In short, insurers are being asked to lift their standards at exactly the point where the evidence shows some are missing the current ones.

We've examined the full evidence base — APRA and AFCA data, ASIC enforcement, the Code monitor's reports and the review documents themselves — in our cornerstone white paper, Are Australia's Life Insurers Ready for LICOP 3.0? This article is the short version, with a focus on what it means if you're considering, or already navigating, a claim.

The full analysis — free to read

Our fully-referenced white paper pulls together the regulatory framework, the APRA/AFCA/Code-committee data, the ASIC enforcement record, and a section-by-section look at what the next Code proposes.

Most people only know about one cover — and it may not be the right one

When money is tight, people reach for the cover they know they have: TPD inside their super. More than 13 million Australians hold TPD cover, almost all of it through superannuation, so for many it is the only insurance they are aware of. But TPD is a strict, permanent-disability lump sum. It is not designed for someone who is off work for a while and needs income now.

You may also hold income protection — monthly payments while you can't work — or have an early-release-of-super option on medical or hardship grounds. Which one fits depends on your situation, not on which product is easiest to find. The Council of Australian Life Insurers has described people being funnelled into TPD when it may not suit them as "a square peg in a round hole."

That is why it is worth checking what you actually hold before you assume TPD is your only move. A free claim check can map the cover in your super — TPD, income protection, death and terminal illness — and which pathway may fit.

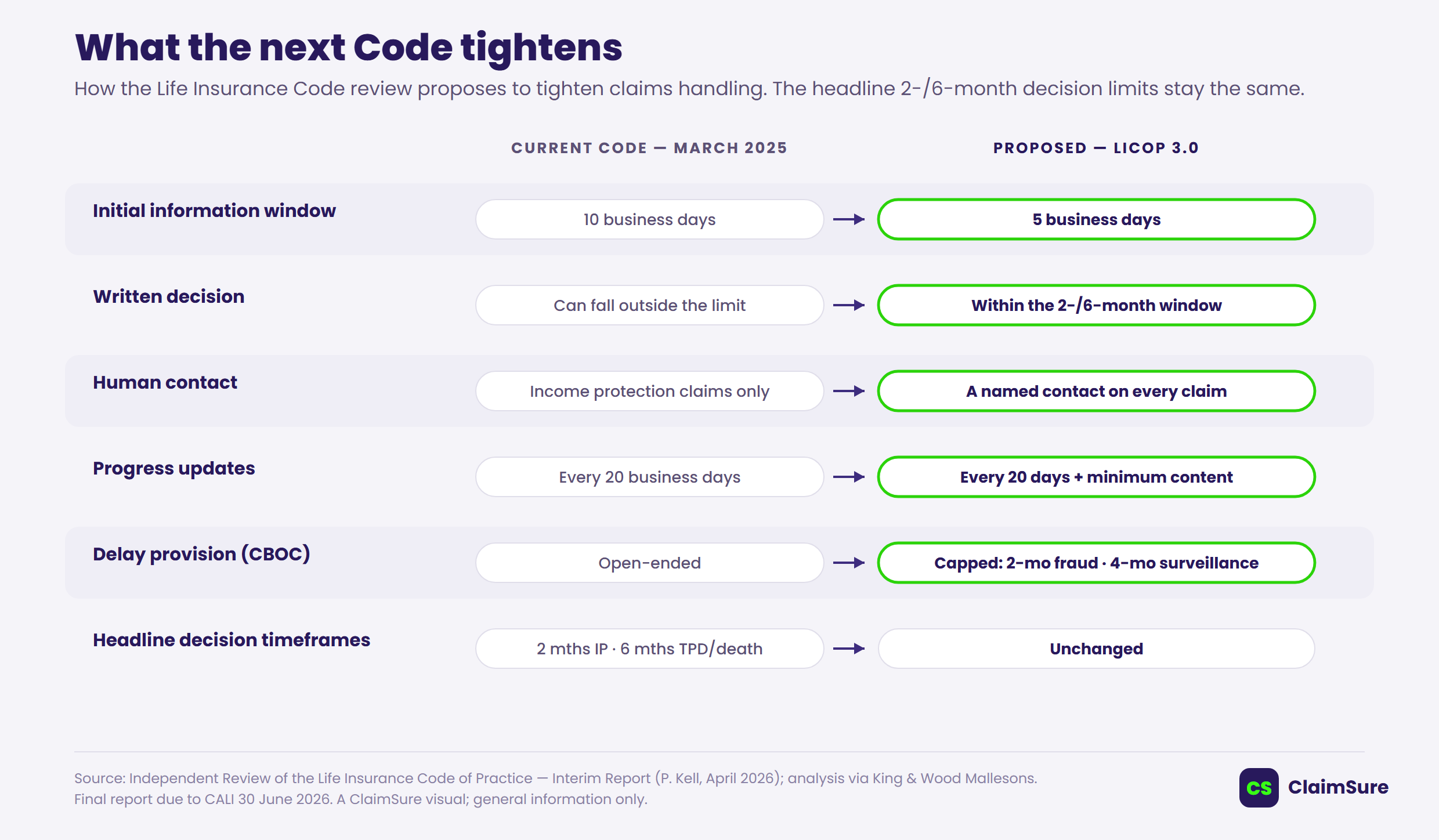

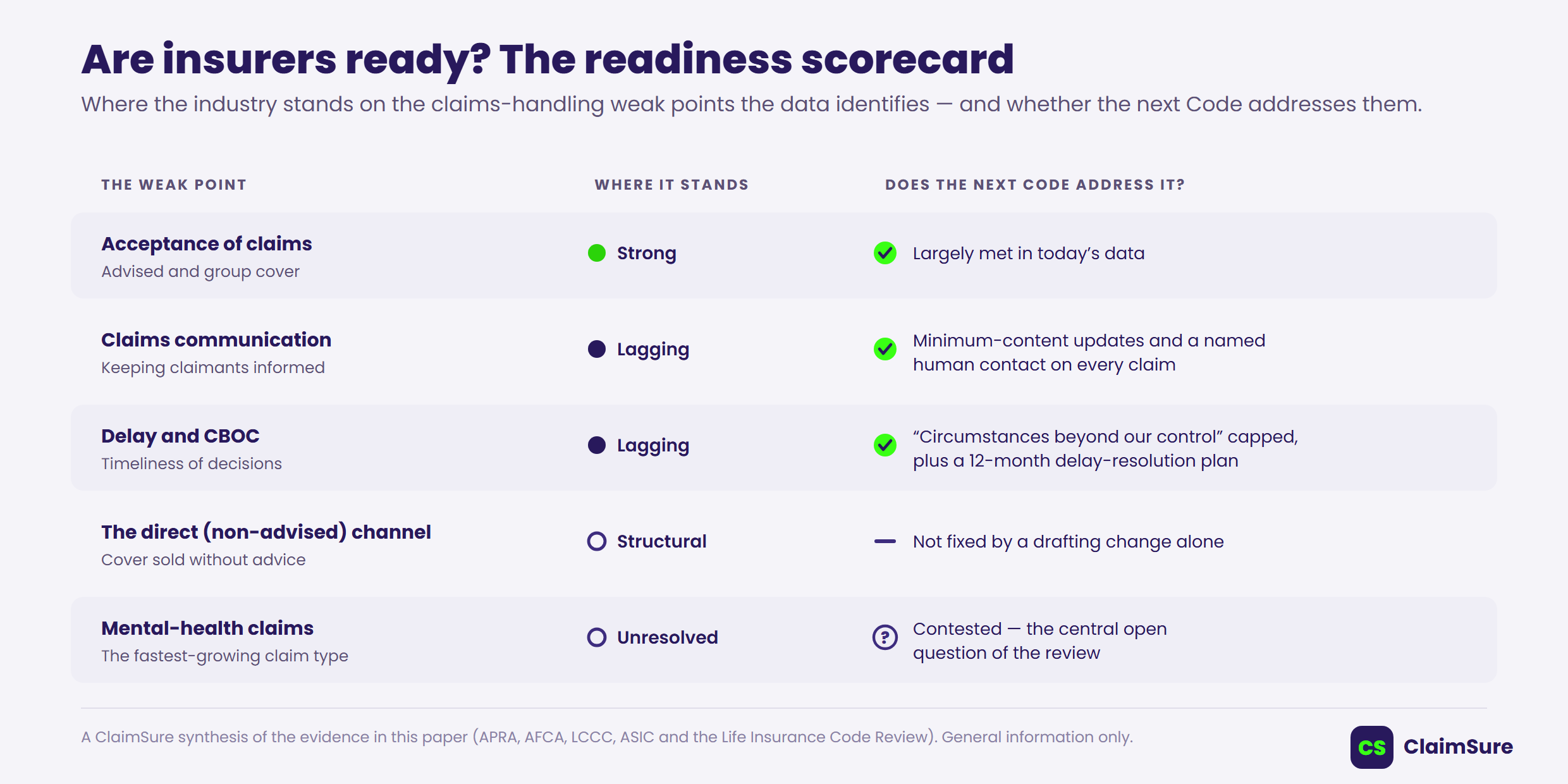

What's actually changing

The headline timeframes stay the same: an insurer still has two months to decide an income protection claim and six months for a lump-sum claim such as TPD or death cover. What the review proposes to tighten is everything around those deadlines. On the reviewer's preliminary recommendations, insurers would have to:

- cut the initial information-gathering window from 10 business days to 5;

- issue the written decision within the overall two- or six-month limit, rather than tacking extra time on the end;

- give every claimant a real, named human contact — not just income protection claimants;

- put minimum substance into progress updates, instead of generic "still in progress" messages; and

- accept tighter limits on the "circumstances beyond our control" provision that has been used to extend claims.

The review also proposes stronger enforcement — letting the compliance committee name insurers in its reports and embedding the Code in customer contracts. Law firm King & Wood Mallesons summed up the direction of travel bluntly: insurers "will need to raise their standards," and should "start a gap analysis now rather than waiting for the final report."

The current gaps the data reveals

Why does this matter for an individual claim? Because the data shows the problems are concentrated in specific, predictable places — and they map closely to TPD and income protection.

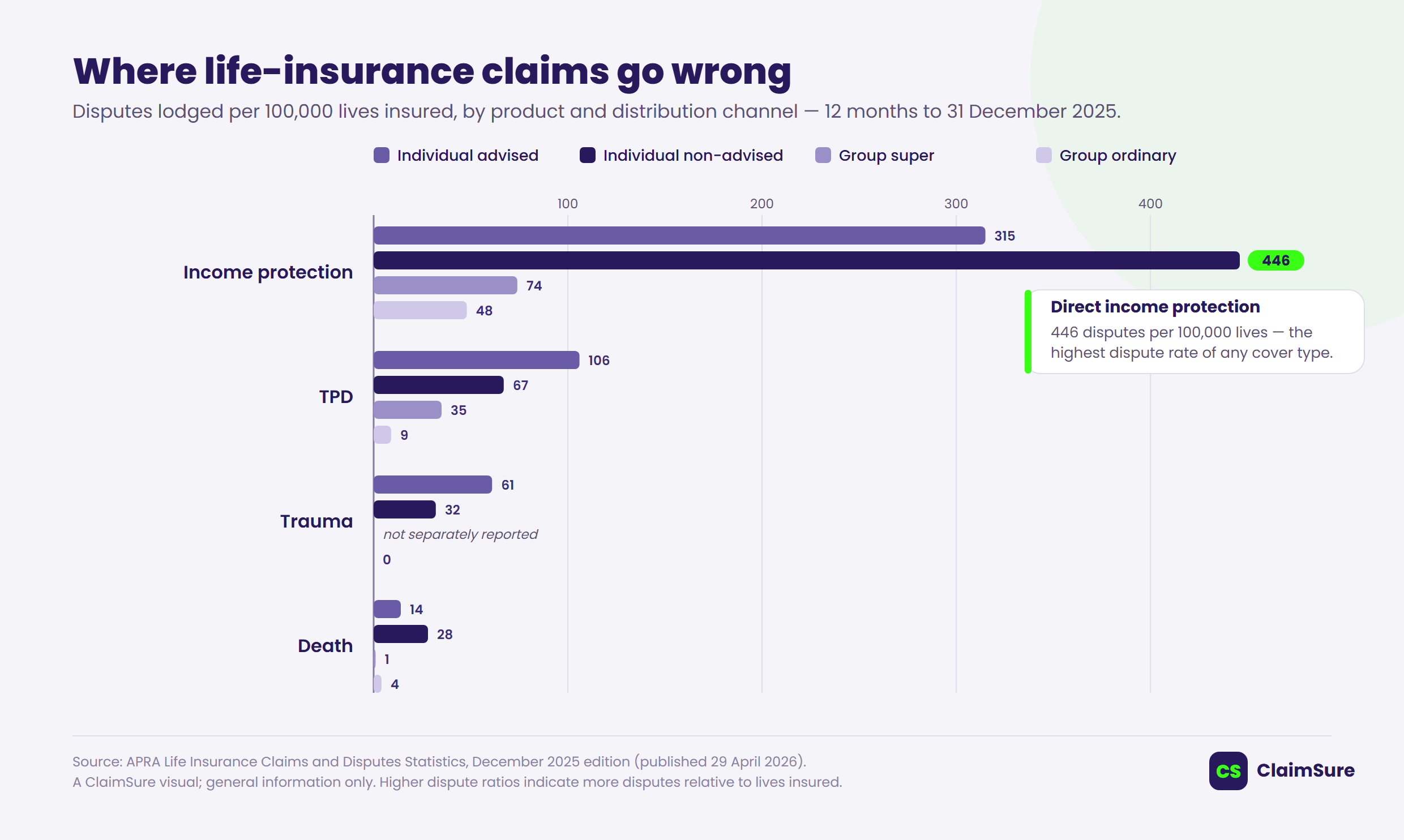

- TPD and income protection generate the most disputes. In APRA's data for the year to December 2025, income protection sold without advice produced 446 disputes per 100,000 lives — the highest of any cover type — and TPD sold without advice had the lowest acceptance rate of any major category, at 69%.

- TPD is the slow product. TPD claims take around 3.8 months on average to finalise, and roughly one in six takes longer than six months.

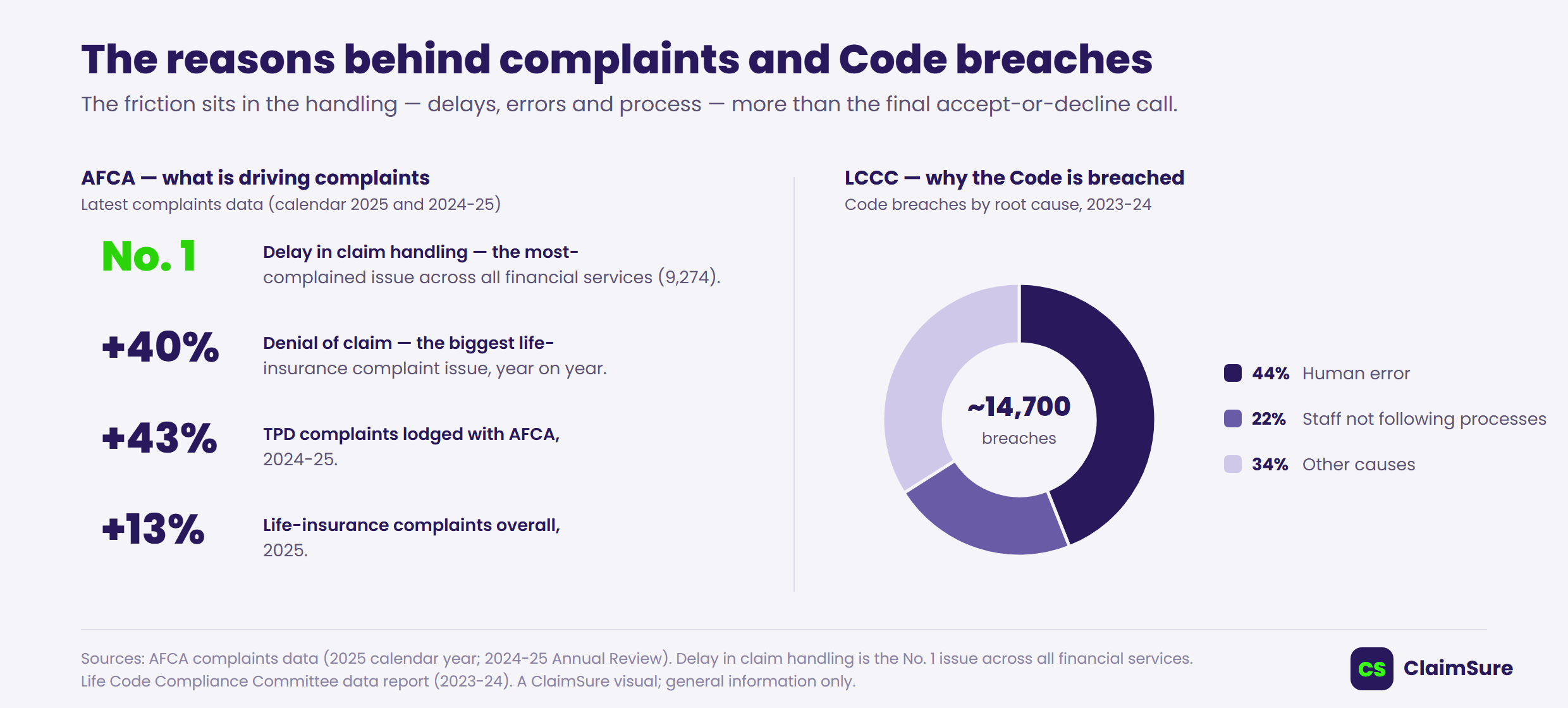

- Delay is the number-one complaint. Across all of financial services in 2025, "delay in claim handling" was the most-complained-about issue at the Australian Financial Complaints Authority (AFCA), and TPD complaints rose 43% over the prior financial year.

- The standard now has teeth. In November 2025 the Federal Court ordered a major super fund's trustee to pay a $23.5 million penalty for failing to handle death and TPD claims "efficiently, honestly and fairly" — with roughly half of open death claims and over a third of open TPD claims left unresolved beyond a year.

And when claims go wrong, it is usually the handling — delay, error and process — rather than the final yes-or-no decision.

The fuller picture, with all the figures and primary sources, is in the white paper.

Why mental health claims are the flashpoint

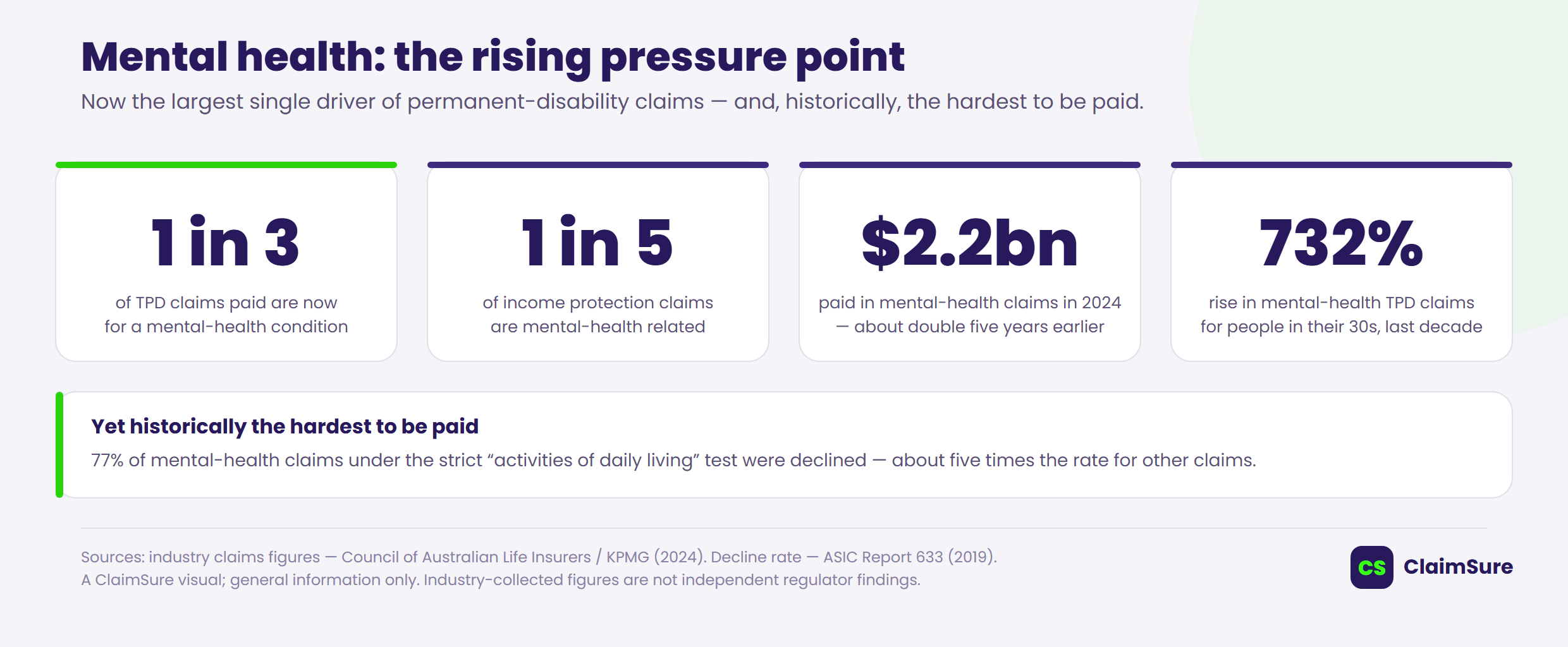

Mental health is now the single largest driver of permanent-disability claims. On the industry's own figures, it accounts for close to one in three TPD claims and around one in five income protection claims. It is also where claims have historically been hardest to get paid — under the most restrictive "activities of daily living" test, ASIC found mental-health claims were declined at a rate of 77%.

That tension — rising claims on one side, restrictive tests on the other — has made mental health the most contested issue in the Code review. The industry wants room to limit mental-health cover in standard policies; the reviewer has warned that doing so could be "a step back" from existing commitments. How it's resolved will shape both the cover people can buy and the claims they can make.

So — are insurers ready?

On the evidence, the answer is qualified. Acceptance rates for advised and group cover are high and improving, but the gaps cluster in claims communication, delay, the direct (non-advised) channel and mental health — the exact areas the next Code is trying to tighten.

For someone with a claim, the takeaway is simple: the parts of the system most likely to go wrong are the handling, the timing and the communication — which is exactly where a second set of eyes can help.

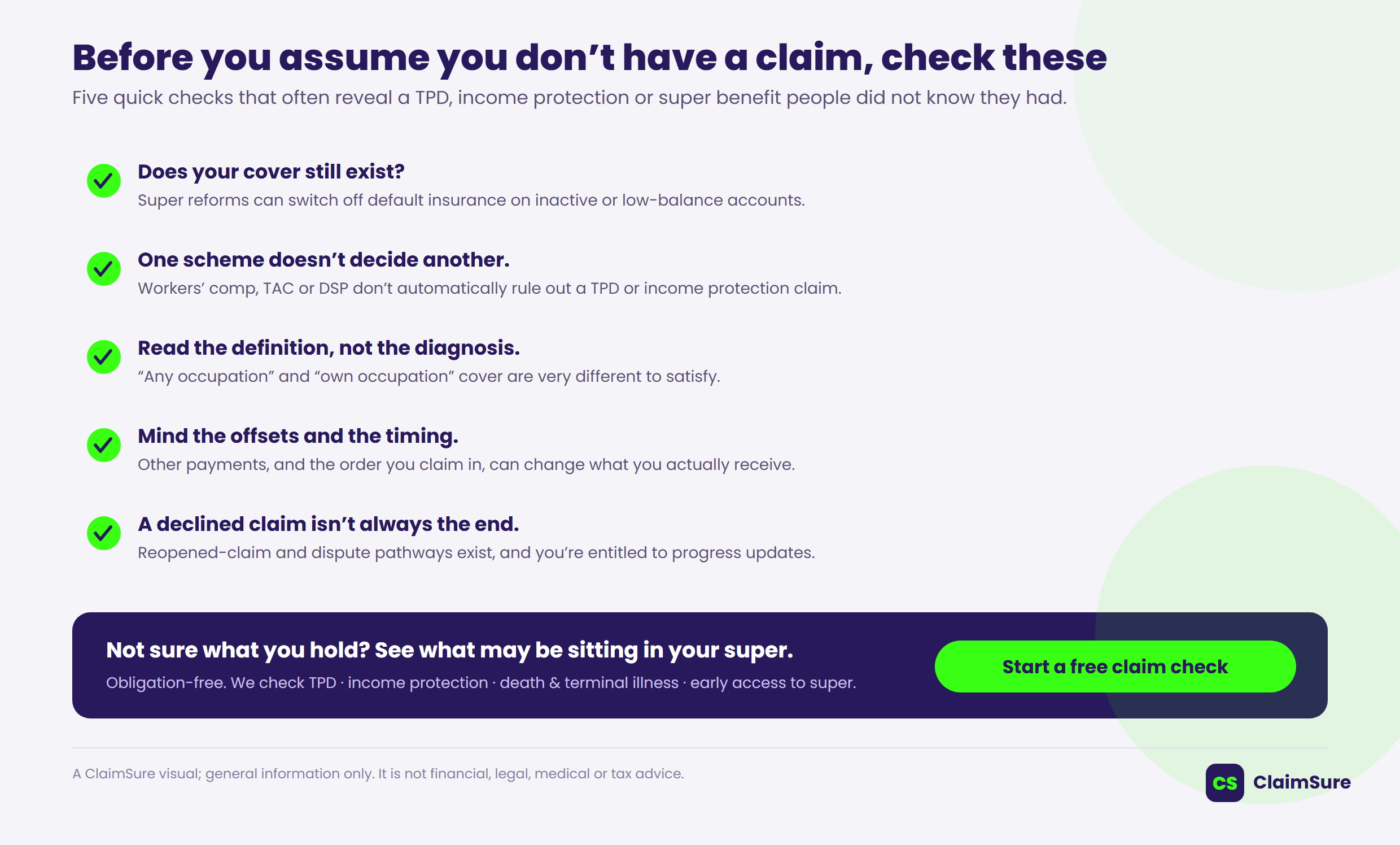

What to check before you assume you do — or don't — have a claim

None of the following is advice, and every situation turns on the specific policy wording, legislation and evidence. But the review and the data point to a handful of things worth checking.

- Check that your cover still exists. After superannuation reforms in 2019–2020, default insurance can switch off on an inactive or low-balance account, or never start for a younger member. Holding a super account is not the same as holding cover.

- Don't assume one scheme's outcome decides another. Being on — or being declined by — workers' compensation, a motor-accident scheme, or the Disability Support Pension does not automatically determine a TPD or income protection claim. Each applies its own test.

- Read the definition, not just the diagnosis. Whether your TPD cover is "any occupation" or "own occupation," and whether a benefit is a lump sum or an income stream, can change both eligibility and how it interacts with other payments. Evidence that you can't do your old job may not, on its own, satisfy an "any occupation" test.

- Mind the offsets and the timing. Income protection benefits can be reduced by other income-replacement payments — such as workers' compensation — depending on the policy wording, and the order in which claims are made can matter.

- A declined claim isn't always the end. Reopened-claim and dispute pathways exist, and you're entitled to regular progress updates on a claim in progress.

Not sure what you actually hold? A free claim check is an obligation-free way to map the cover you may have — including TPD, income protection, death and terminal illness, and early access to super.

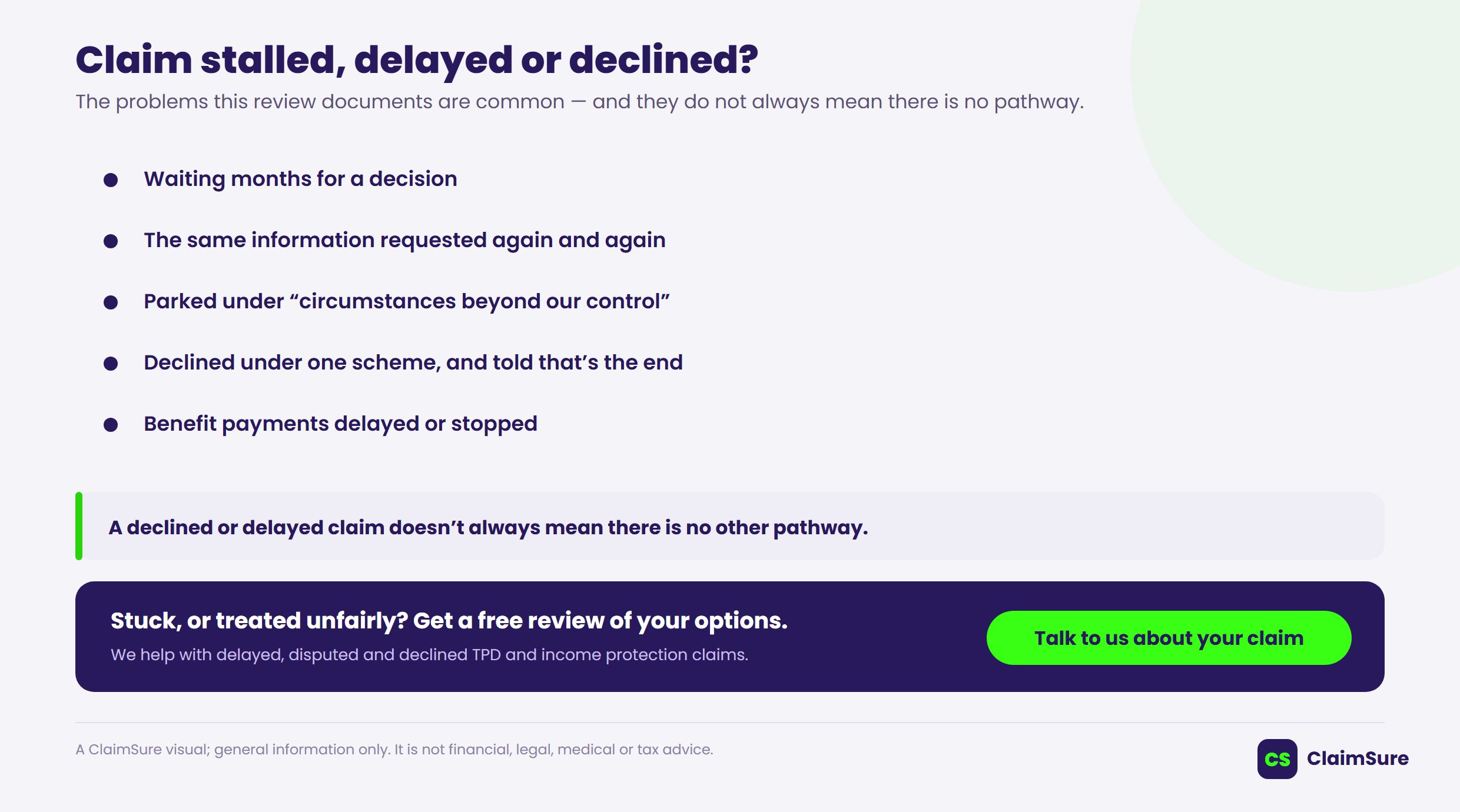

Already stuck in a delayed or declined claim?

The friction this review documents — months of delay, the same medical information requested again and again, claims parked under "circumstances beyond our control," a decline that you were told was final — is exactly what many people are living through right now. It does not always mean there is no pathway.

A decision in one system, such as a Centrelink or workers' compensation decision, is not the same as an insurance decision, because they use different rules. If your claim has stalled, been disputed or been knocked back, it may be worth a second look at how it was handled and whether another pathway is open.

Talk to us about a delayed or declined claim →

Read the full analysis

This article is a summary. For the complete, fully referenced review — including the regulatory framework, the APRA, AFCA and Life Code Compliance Committee data, the ASIC enforcement record, and a section-by-section look at what the next Code proposes — read our cornerstone white paper:

This article provides general information only. It does not take into account your personal circumstances and is not financial, legal, medical or tax advice. Claim eligibility depends on the relevant policy wording, legislation, medical evidence, employment history and individual circumstances.

Sources and further reading

- ClaimSure white paper, Are Australia's Life Insurers Ready for LICOP 3.0? (2026) — the cornerstone analysis and full reference list.

- Independent Review of the Life Insurance Code of Practice — Interim Report (Peter Kell, April 2026); final report due to CALI 30 June 2026. lifecodereview.org.au

- APRA, Life Insurance Claims and Disputes Statistics (data to December 2025). apra.gov.au

- AFCA, complaints data 2025 and 2024–25 Annual Review. afca.org.au

- ASIC, 25-286MR — Cbus $23.5 million penalty (November 2025); Report 633 — Holes in the safety net (2019). asic.gov.au

- CALI, Mental ill health is straining Australia's safety net (2025). cali.org.au

A free claim check with ClaimSure

ClaimSure helps people understand the claims they may be able to make through life insurance and superannuation — including TPD, income protection, and death or terminal-illness cover — and how those claims interact with other systems such as workers' compensation, motor-accident schemes and Centrelink. A free claim check is an obligation-free conversation; it does not guarantee any outcome, and eligibility always depends on the relevant policy wording, legislation, medical evidence and individual circumstances.

Start a free claim check →