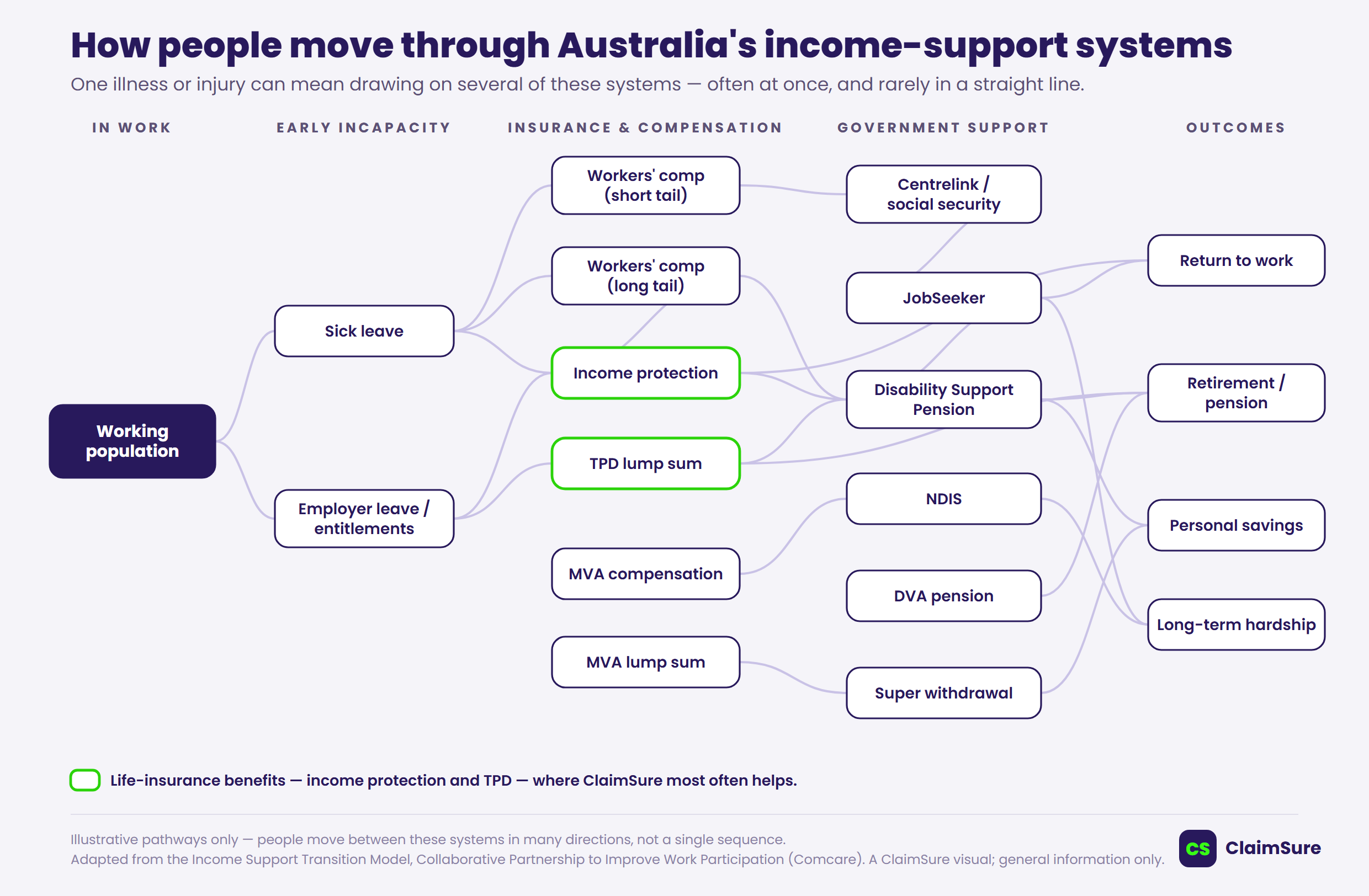

Australia does not have one safety net. It has many.

When someone becomes too unwell or injured to work, most people assume there is a clear pathway for support. In reality, the system can be far more complicated. A person may deal with sick leave, workers compensation, TAC or motor accident compensation, income protection, TPD insurance, Centrelink, DSP, early access to super, private health providers, rehabilitation providers, employers, super funds and insurers — sometimes at the same time.

Multiple schemes form a fragmented safety net. That is the key issue highlighted by recent research into Australia's income support ecosystem. The research maps how different systems interact when people are unable to work due to illness, injury or disability — and shows why many Australians struggle to understand what they may be entitled to, when to apply, and how one claim can affect another.

The Income Support Transition Model, developed through the Collaborative Partnership to Improve Work Participation, maps ten major income and benefit support systems, including workers compensation, life insurance income protection, life insurance TPD, social security, superannuation withdrawal and motor vehicle accident compensation. It was designed to show how decisions in one system can affect other systems.

Why this matters now

Newer research commissioned by the Council of Australian Life Insurers and prepared by SuperFriend found that around 8.5 million Australians accessed some form of income support in the past year, at a total cost of $78.9 billion. The report also found that mental ill-health is now a major driver of claims — around one in three TPD claims and one in five income protection claims. In 2023–24, life insurers alone paid $8.3 billion in income protection and TPD benefits to about 55,000 people who could not work — roughly 11% of all income support across the mapped systems.

The pressure is not limited to one scheme. Claims are rising across government, employers and insurers. CALI has also noted that life insurers often become involved later in a person's income support journey, after they have already moved through other parts of the system.

That is exactly what ClaimSure sees in practice. Someone may start with sick leave, then move to workers compensation or TAC, then apply for income protection, then consider TPD, early release of super or DSP. Each scheme has its own rules, evidence requirements, definitions and timeframes. There is no single front door.

TPD, income protection, workers compensation and TAC can overlap

Many people are surprised to learn that being on one type of claim does not automatically stop them from having another potential claim. For example, depending on the legislation and the policy wording, a person may have:

- a workers compensation claim for a work-related injury or illness;

- a TAC or motor accident claim if their incapacity relates to a transport accident;

- an income protection claim through super or a retail policy;

- a TPD claim through super;

- a Centrelink or DSP pathway;

- a possible early access to super application on medical or financial hardship grounds.

These systems are connected, but they are not the same. A workers compensation claim may focus on whether an injury arose out of or in the course of employment. A TAC claim may focus on a transport accident. Income protection usually looks at whether you are unable to work under the policy definition and may include offsets for other payments. A TPD claim usually looks at whether you are unlikely to return to suitable work, based on your education, training and experience. DSP has its own social security rules and medical criteria.

That means a person may be accepted by one system, delayed by another, or rejected by one system while still having a valid pathway elsewhere. The problem is not just eligibility. It is navigation.

The research shows that Australia's income support systems are interrelated, but many people experience them as disconnected. Comcare describes the income support transition model as a way to understand the "complex behaviours, relationships and transitions" between systems and how a decision in one system can affect another.

For the person dealing with the illness or injury, this can mean:

- repeating the same medical history to different organisations;

- asking doctors to complete similar forms in different formats;

- waiting months for decisions;

- not knowing whether to apply for IP, TPD, DSP or early access to super;

- worrying that one claim will damage another;

- not knowing whether workers compensation or TAC evidence can support a super insurance claim.

This is where people often get stuck. They may have insurance through super but assume workers compensation is their only option. They may be receiving TAC or WorkCover payments and not realise they also hold TPD cover. They may be declined for one benefit and assume that means every other pathway is closed. That is not always correct.

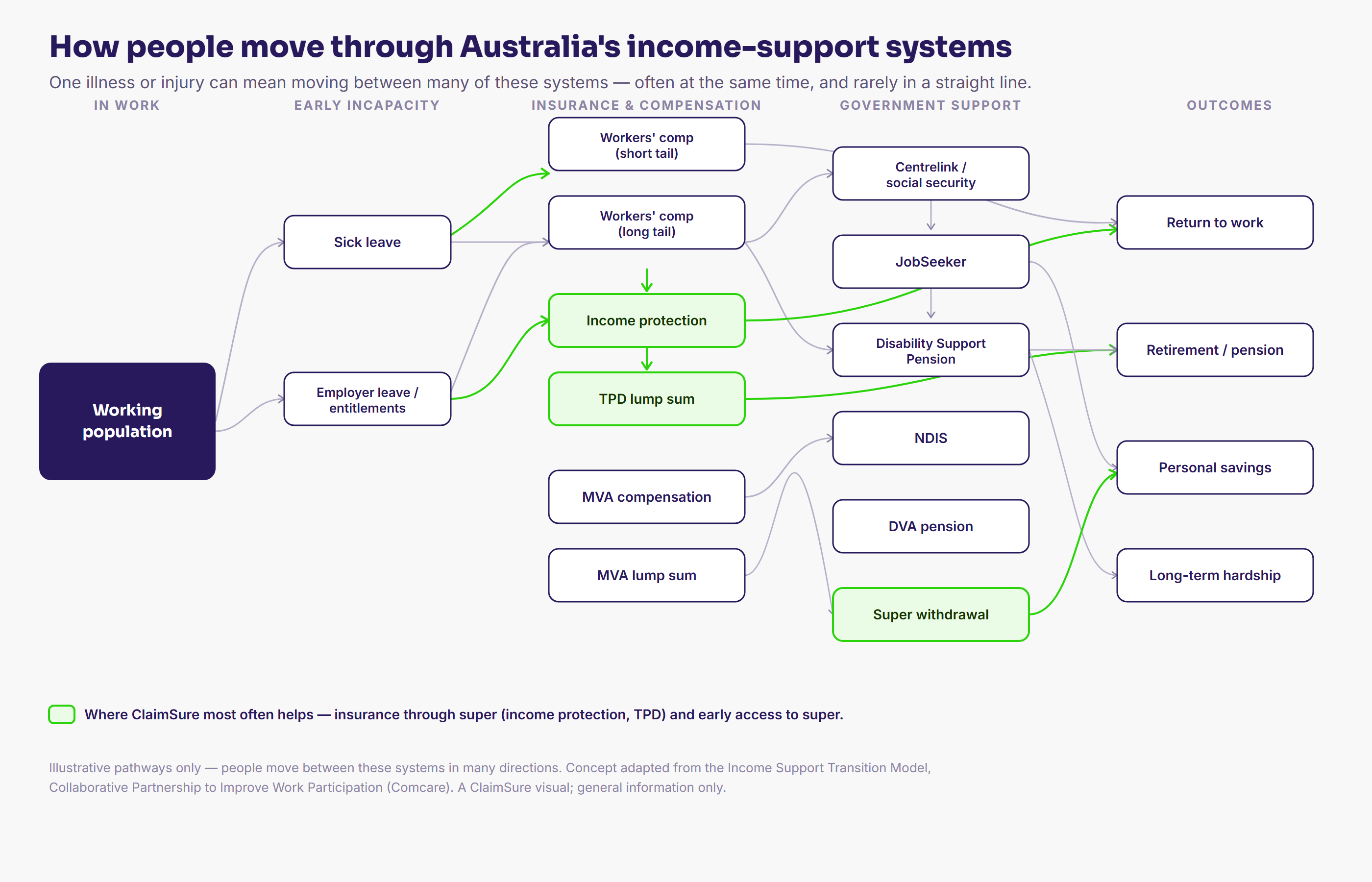

Case study: one person, four systems

The Collaborative Partnership's factsheet shares the example of "Patricia," a 52-year-old aged-care worker who developed chronic, disabling back pain caused by her work. On her journey back to employment she moved through four different income-support systems — employer entitlements, then workers' compensation, then (because of long wait times) Newstart/JobSeeker at around 25% of her previous income, before claiming a TPD lump sum. Her re-employment journey took four years.

It's a clear illustration of how one injury can mean navigating several systems at once — and why it's worth checking every pathway, including any insurance inside your super. Source: Collaborative Partnership to Improve Work Participation — Model factsheet (Comcare).

Why policy wording matters

The interaction between claims depends heavily on the wording of the policy, the legislation behind the scheme, and the medical and employment evidence available. For example:

- Income protection may be affected by other income payments. Some policies reduce benefits if the person is receiving workers compensation, TAC, Centrelink or other income replacement payments.

- TPD is different. A TPD claim is usually a lump sum claim based on permanent incapacity and the policy definition. A person may still be able to pursue TPD even if they have been involved in workers compensation, TAC, Centrelink or other systems.

- Workers compensation and TAC evidence may help show the history of incapacity, treatment, rehabilitation attempts and work restrictions. But the insurer may still apply its own TPD or income protection definition.

- DSP and Centrelink decisions may be relevant, but they are not the same as an insurance decision. Centrelink uses social security legislation. Insurers use policy wording.

- Early access to super is also separate. Accessing super early due to permanent incapacity, severe financial hardship or compassionate grounds does not automatically mean an insurance claim has been assessed or paid.

This is why it is risky to assume there is only one pathway.

A fragmented system can leave people missing support

The CALI and SuperFriend research describes Australia's income support system as a broader ecosystem made up of multiple schemes, including employer sick leave, workers compensation, life insurance, social security, motor vehicle accident compensation, veteran entitlements and early access to super.

But for everyday Australians, the issue is simple: when you are sick or injured, you do not want a system map. You want to know:

- What can I claim?

- What cover do I have?

- Will one claim affect another?

- What evidence do I need?

- What happens if I have already been declined?

- Who is supposed to help me navigate this?

That is the gap ClaimSure is designed to help with.

You may have more than one pathway

If you have stopped work or reduced work because of illness, injury, disability or mental health, it may be worth checking whether you have insurance or support options you have not yet considered. This can include:

- TPD insurance through super;

- income protection through super;

- retail income protection or trauma cover;

- workers compensation;

- TAC or other motor accident compensation;

- early release of super;

- DSP or other Centrelink support;

- options if a claim has been delayed, declined or closed.

You do not need to know the answer before asking for help. A free claim check is designed to identify whether there may be a pathway worth exploring.

ClaimSure can help you check your options

Australia's income support system is not simple. The research makes that clear. Different schemes can overlap. Different definitions can apply. One claim may influence another. A declined claim does not always mean there is no other pathway. And a person may have insurance through super without realising it.

If you are dealing with illness, injury, disability, mental health issues, time away from work, workers compensation, TAC, Centrelink or a possible TPD claim, ClaimSure can help you take the first step.

Start with a free claim check. We can help you understand whether there may be a claim pathway worth exploring, what information may be needed, and whether your super insurance, work injury claim or other support systems may interact.Sources & references

- Collaborative Partnership to Improve Work Participation — Income Support Transition Model / cross-sector project report (Comcare).

- Collaborative Partnership to Improve Work Participation — Model factsheet, including the "Patricia" case study (Comcare).

- Council of Australian Life Insurers (CALI) & SuperFriend — Cross Sector Project Update: Mapping Australia's ecosystem of income supports (2026): around 8.5 million Australians accessed income support in the past year, totalling $78.9 billion.

- Moneysmart (moneysmart.gov.au) — insurance through super: life, TPD and income protection.

- Australian Taxation Office (ato.gov.au) — finding and consolidating lost or forgotten super.

This article provides general information only. It does not take into account your personal circumstances and is not financial, legal, medical or tax advice. Claim eligibility depends on the relevant legislation, policy wording, medical evidence and individual circumstances.

Start with a Free Claim Check

Not sure which pathway applies to you? Reach out and we'll review your circumstances together — no obligation, plain English.

Free Claim Check →