New research released by the Association of Superannuation Funds of Australia (ASFA) suggests that since the 2019 super reforms, thousands of Australians and their families have been missing out on billions of dollars in life and disability insurance benefits — often without ever realising they had lost their cover.

The findings, presented at ASFA's Spotlight on Insurance forum in Sydney on 5 March 2026, put numbers to a problem ClaimSure sees regularly: people who assume they have no insurance, when in fact their cover was quietly switched off.

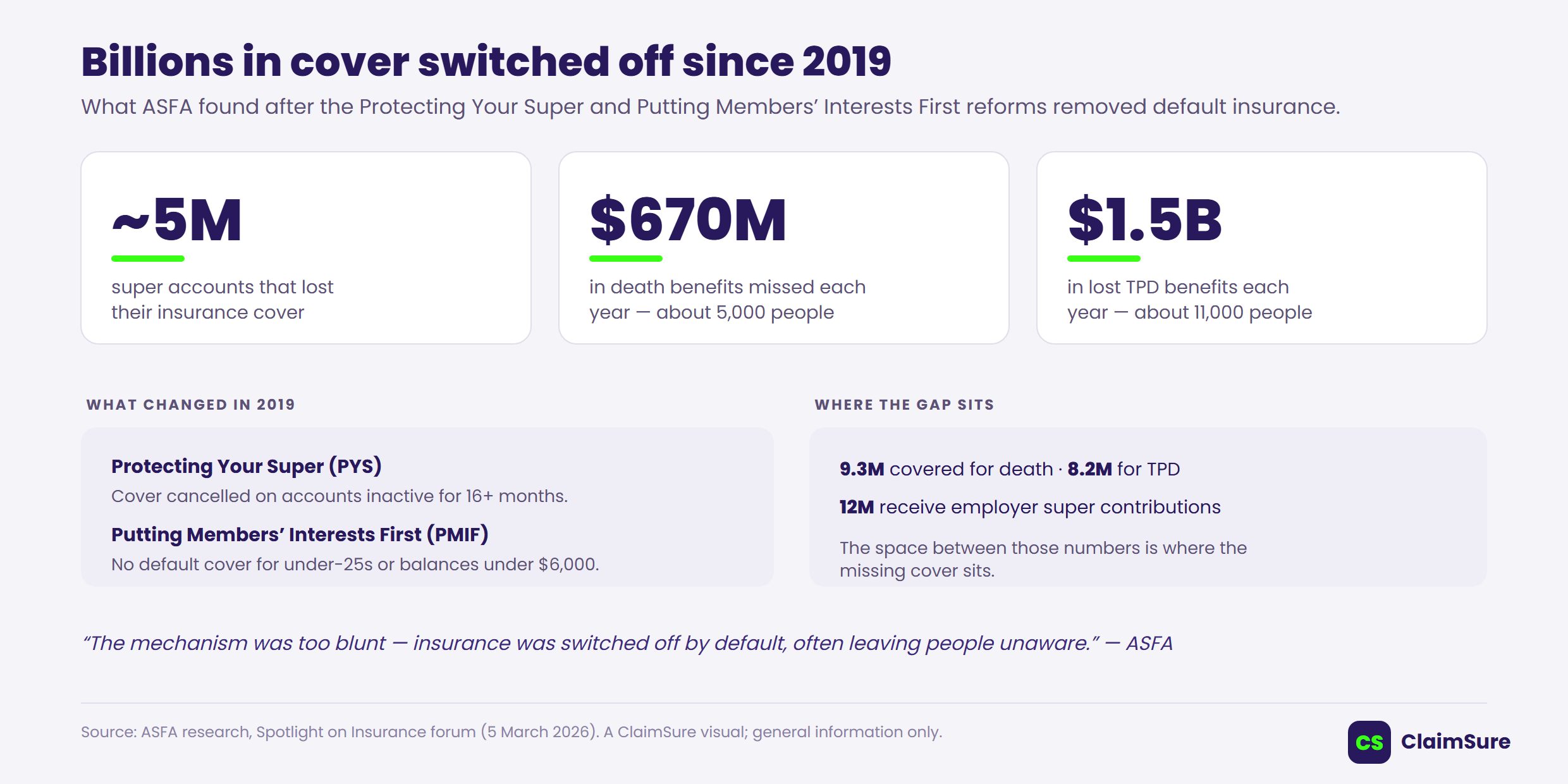

The key numbers

Source: ASFA research, Spotlight on Insurance forum, 5 March 2026.

What changed in 2019

Two reforms changed how insurance works inside super. The Protecting Your Super (PYS) package required funds to cancel insurance on accounts that had been inactive — that is, had not received a contribution — for 16 months or more. The Putting Members' Interests First (PMIF) Act then removed automatic, or "default," insurance for members under 25 and for accounts with a balance below $6,000.

The intent was reasonable: stop people paying premiums on low-balance or duplicate accounts they had forgotten about, which was quietly eroding their retirement savings. But ASFA's research suggests the change went further than many people understood.

The headline numbers

According to the ASFA research, the reforms led to around 5 million super accounts losing their insurance cover. The flow-on effect, year after year, is significant:

- An estimated 5,000 Australians a year have died without the life insurance they might otherwise have held through super.

- That equates to roughly $670 million in death benefits not reaching families each year.

- Around 11,000 people a year are estimated to be missing out on total and permanent disability (TPD) benefits.

- That represents about $1.5 billion in lost TPD benefits annually.

For context, ASFA notes that around 9.3 million Australians are currently covered for death benefits through super and 8.2 million for TPD — while roughly 12 million receive employer super contributions. The gap between those figures is where the missing cover sits.

"The mechanism was too blunt"

ASFA's view is not that the reforms were the wrong idea, but that the way cover was removed was indiscriminate. As the association's Chief Policy and Advocacy Officer put it, "The mechanism was too blunt. Insurance was switched off by default, often leaving people unaware it had happened."

That last point matters most for everyday members. Many people never received — or never absorbed — the message that their cover had ended. They only find out at the worst possible time: when they, or their family, need to make a claim.

Who is most affected

The research points to several groups who are most likely to have lost cover, or never had it switched on in the first place:

- workers under 25

- people with low super balances (under the $6,000 threshold)

- self-employed people whose accounts became inactive

- younger workers and anyone who had not yet reached the minimum balance for default cover

People who change jobs often, take career breaks, or hold more than one super account are particularly exposed, because their accounts are the most likely to tip into "inactive" status and have insurance cancelled.

What ASFA is recommending

To close the gap, ASFA has put forward several policy changes, including:

- extending opt-out insurance to members aged 21 and over, rather than 25

- applying default cover to new full-time employees from their first day of work

- replacing automatic cancellation with a stronger opt-out process that requires an active, informed decision from the member before cover ends

It is worth noting that, where cover does exist, the insurance is generally delivering. ASFA points to group TPD and disability income claims-paid ratios above 100% and claim admittance rates in the mid- to high-90% range — in other words, the problem is people not having cover, not insurers refusing to pay.

Why this matters for you right now

Policy changes take time. But you do not have to wait for them to find out where you stand. If you stopped working because of illness or injury, or you are unsure whether your super still includes insurance, the most useful thing you can do is check — and check soon, because inactive accounts can lose cover quietly.

The key things to confirm are:

- whether you have (or had) life, TPD, or income protection cover in any super account

- whether that cover was active at the time you stopped work or became unwell

- whether you have old or lost super accounts that may have held cover

- what definitions and exclusions apply to any policy

Free Claim Check

At ClaimSure, we help people work out whether they may have a potential life insurance claim or support pathway through their super — including in situations where cover may have been cancelled or was never switched on.

We can help you:

- review your situation in plain English

- identify relevant super accounts, including lost or forgotten super

- understand whether there may be TPD, life insurance, income protection, or early access to super options worth exploring

Start with a Free Claim Check

Wondering if any of this applies to your situation? Reach out and we'll review your circumstances together — no obligation, plain English.

Free Claim Check →